This December, Silk Road continues. Four days of exhibitions, talks, presentations, dinners, bringing together artists, collectors, curators, and cultural thinkers.

I was talking to a gallerist earlier this year about onboarding more collectors into the digital art space. At some point I asked him, half-joking, “So who’s going to be buying my bags in the future?”

“You will.”

I laughed. He didn’t lol. Maybe it was the French bluntness, maybe he genuinely meant it forward. And the longer I’ve thought about it, the more it makes sense. We are buying our own bags and that’s not a bad thing. “We” are growing in purchasing power, in cultural influence, and in relevance. As I’ll touch on in a bit, this adoption we’re looking for is coming from people around us; they’re probably not in Mayfair.

For years, there’s been this collective expectation that traditional collectors will eventually sweep in and legitimise digital art through sheer capital. And look, some of them will come in. They already are, in small but meaningful ways, and the ones who do tend to be genuinely curious about the tech, the culture, or the artists themselves. But I also understand why the broader wave of ‘sophisticated’ capital hasn’t arrived yet. The system is built around them and works perfectly fine for what they want, and also serves their interests.

So the question becomes: who actually moves the needle for digital art?

Over the last few months, I’ve been digging through different reports, data points, and conversations, trying to get a clearer sense of how different collector demographics are behaving. The more I look, the more it feels like the momentum is quietly shifting in a direction that really favours digital art.

The Dream Of a Colonial Battle Flag/ Grand Epitaph Luc Zeshawn 2023

1. Younger collectors don't trust the traditional art market

This keeps showing up in every report I come across, and it mirrors what I hear in real conversations. Younger collectors often look at the traditional gallery system and feel like it wasn’t built with them in mind. Undisclosed pricing, insider lists, waitlists, preferential treatment for long-standing clients — the whole thing can feel like a closed circuit, something you can admire from the outside but not easily step into. It’s no surprise that 69% of young collectors say a lack of transparency has stopped them from buying art entirely (Artsy).

In the digital art world, we’ve unintentionally solved parts of this. Not because anyone set out to ‘fix the art market’, but because the tools we use, on-chain provenance, public price histories, visible ownership, fewer gatekeepers, naturally create a more open environment. Artists can actually see (most of the time) who collects their work. Collectors can trace the sales provenance. Yes, royalties remain messy, and yes, web3 has developed its own versions of gatekeeping. But the foundation and intentions are there. We’ve built infrastructure that can be fair, which is already more than what many younger collectors feel they get elsewhere.

In the long run, this transparency is exactly what serves digital art. New collectors don’t want to navigate a maze just to buy something they love. They want clarity, context, and a sense that the system isn’t stacked against them. Digital art provides that by default. As younger generations take on more cultural and financial influence, they’re going to expect openness and accessibility and digital art already aligns with that expectation.

A Prophetic Warning Keke 2025

Blind Supper Keke 2025

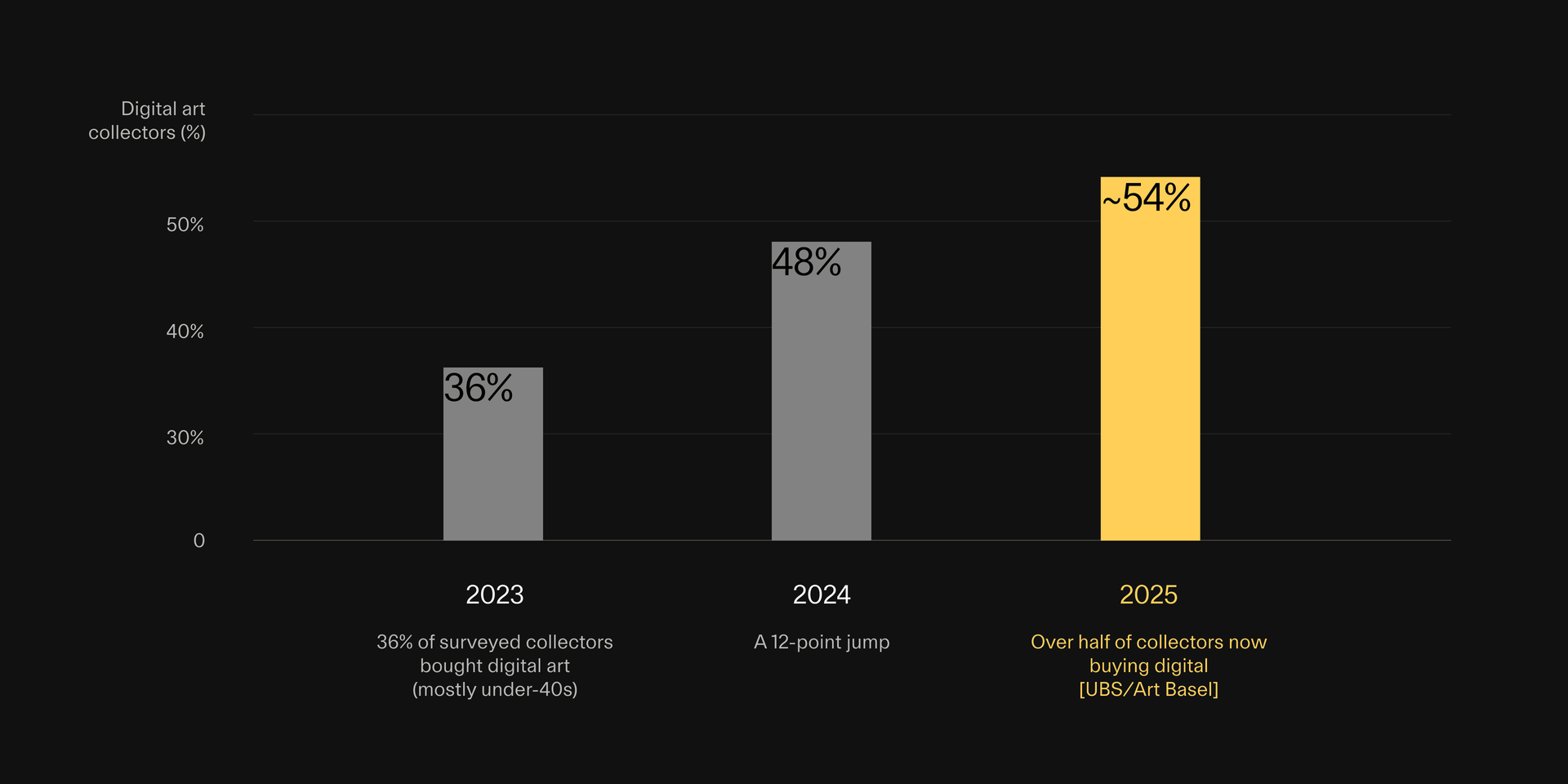

2. Collector behaviour favours digital

If you look at the UBS Art Market Reports from 2023 to 2025, there's a clear trajectory:

Meanwhile, traditional channels are losing ground. In-person auction participation is down 25 percentage points since 2023 [UBS 2025]. Younger collectors prefer online pathways, even when buying physical art. According to Avant Arte, collectors aged 18-39 overwhelmingly prefer digital formats and digital-first experiences, the inverse of older demographics.

What this really tells us is that the next generation of high-intent buyers is already self-selecting into digital. The new generation of collectors entering the market today, those in their 20s, 30s and early 40s grew up online, their cultural references live online and their first major purchases often happen online.

As this cohort matures and their earning power increases, they’ll become a primary force behind global art spending. This is how digital art becomes less of a niche and more of an inevitability.

Though they’ll continue to attend art fairs and other IRL events, their primary discovery tool will be Instagram and other social media platforms. They’ll continue to buy physical works, but the jump to digital will not be alien to them. Context, provenance, immediacy, transparency and cultural relevance will be the criteria that determines what gets collected and why. It’ll be down to us to provide that for them; I somehow don’t see Christies doing it.

Of course it’s easy to get caught up in the little echo bubble on Twitter, and there is a great deal of apathy amongst digital art collectors. Yet under the surface, there is a growing demographic that is ready for what we have to offer.

The trend is in our favour, anon.

Infinite Images ∞ 83 Holly Herndon & Mat Dryhurst 2024

3. Collecting is becoming identity curation

Younger collectors, myself included, think a lot about what our art says about us. It’s not just buying something beautiful; it’s buying something that feels like an extension of who we are.

Seventy-three percent of under-35s say they collect art that reflects their identity (Avant Arte), and more than half say their very first purchase wasn’t about financial upside at all, it was about emotional or cultural alignment. People want their collections to feel personal, expressive, and rooted in what they care about.

This is true in my case. I like people seeing what I collect. I want them to understand the aesthetics that resonate with me. When someone sees that I collected Mika Ben Amar’s Internet Flowers, for example, it isn’t just about the artwork. It’s because I genuinely believe privacy has become one of the defining issues of our time, and that piece captures something essential about the moment we’re living in.

Some of my favourite works in my collection are physical pieces, but they come with a completely different set of challenges. I have to think about where to hang them, how to store them, what room they live in. I have a deep personal relationship with these works, but part of me also wishes my friends online could experience them too. They’re meaningful to me, but unless you visit my home, you’ll never see them.

That’s where the mechanics of digital art feel different. When something lives on-chain, can be shared on social feeds, displayed on screens, or seen through a public wallet, it naturally fits how we already express ourselves. Digital art moves through the same channels where identity lives today, so showing someone your collection isn’t a logistical puzzle, it’s as simple as sharing a link.

survive at all cost TJO 2023

Collecting is slowly becoming less about what you hang in your home and more about what you show the world. Younger buyers, especially, want to signal their taste, their values, the groups they align with. Online galleries, wallet profiles, online communities, they all give collectors a way to express themselves in real time.

That said, the digital art space isn’t perfect yet. There are still real challenges around UI/UX, and the lack of industry-standard digital products that make onboarding new collectors truly seamless. These are problems that need solving and they’re very much on the agenda but the direction of travel is clear. The behaviour is already there; the infrastructure is playing catch-up.

4. Asia holds the real upside

Collectors in Asia are more than twice as likely to buy digital art compared to the US or Europe, according to the UBS/Art Basel reports. And honestly, it makes sense. Go to Shanghai, Seoul, Hong Kong, Tokyo… you realise very quickly that digital culture just carries more weight there. Screens, online identity, gaming, fandoms, virtual goods, live streams are everyday habits, far more present and normalised than in most Western cities.

The numbers also back it up.

Globally, digital art makes up around 13 percent of Gen Z collections, but UBS and Art Basel’s data shows the share is significantly higher across Asia. Deloitte’s Art & Finance research goes even further, identifying Asian collectors under 35 as the most likely demographic in the world to collect NFTs, AI art and digital media. China alone accounts for roughly 40 percent of global online art sales, more than double the share in Europe, according to UBS. Last data point I’ll touch on, collectors under 40 in Hong Kong, Taiwan and South Korea now represent the largest group of high-spending buyers anywhere in the world.

surround Joe Pease 2024

So what's the point of all this data? For me, it confirms something we’ve been speaking about at SILK for a while. There's already a market primed for digital art, it's just uneven. Most of the noise, the discourse, the “push" is coming from the West. But the behaviours that actually support a thriving digital art market? They're far more present in Asia. The collectors are here. The spending power is here. The cultural alignment is here.

What's missing is cohesion. Right now it feels fragmented. A market waiting for someone to connect the dots.

This is why we’re placing an emphasis on Asia in 2026 and beyond. We’ve been meeting contemporary art collectors in Jakarta, Bangkok, Hong Kong who are curious about digital mediums but don’t quite know how to step into the wider digital art market. Our goal is to bridge that gap to be on the ground, to build relationships, and to make this space feel accessible rather than intimidating.

<div style="height: 50px; width: 100%;"></div>

Work to be done

The trends are leaning in our favour. The behaviours are there, the curiosity is there, the spend is increasingly there. What's missing is the connective tissue, tools and products that don't require a manual. Platforms that feel intuitive, welcoming, familiar to someone buying their first digital artwork. And a social presence that reaches beyond our own echo chambers. Not just Twitter, but also Instagram, TikTok, and other places where the next generation discovers culture.

SILK’s presence at art fairs and IRL events will always matter. But there's a huge world online that barely knows we exist and many of them are already primed to take their first step into digital collecting. The on-ramps are more of a problem than the demand, imo.

This is why the timing feels right to me. We have a digitally native collector base that's growing in confidence, taste, and purchasing power. A whole generation that primarily buys digitally, is ready to buy digital art too.

And with $84 trillion set to pass to younger generations over the next two decades, the centre of gravity is shifting.

TLDR, we are buying our own bags, and soon our friends will too.